Deal Snapshot

- Specialty: Ophthalmology (Cataract, LASIK, Retina)

- Market: Southern California

- Deal Timeline: 9 months (engagement to close)

- Effective Return: 17x EBITDA (cash + rollover appreciation)

- Structure: Practice valuation + ASC co-investment + stock rollover

The Challenge

The physician-owner had built a premier ophthalmology practice over 20+ years—strong EBITDA, excellent payer mix, established referral networks, and a minority stake in an ambulatory surgery center. He was approached directly by a national eye care platform looking to expand into the Southern California market.

The initial offer looked attractive on the surface: 6.5x EBITDA for a 40% stake, with standard earnout provisions. But the owner knew there was more value to capture—if the deal was structured correctly.

The Strategic Approach

Rather than accept the initial terms, the practice engaged institutional M&A advisory support to:

- Unbundle the value streams. The practice, the ASC stake, and the platform growth potential were each distinct sources of value—and should be priced separately.

- Run a sell-side Quality of Earnings (QofE). Engaging a third-party accounting firm to validate EBITDA before buyer due diligence eliminated the typical 10-15% "chip" that buyers take during diligence.

- Model the rollover economics. Rather than taking 100% cash at close, the physician rolled a significant portion into platform equity—betting on the buyer's exit multiple.

The Retrade Defense

Midway through due diligence, the buyer attempted a classic "retrade"—revising the offer terms to reduce upfront cash and increase the employment obligation. This is common in healthcare M&A: buyers know sellers are emotionally invested and rarely walk away this late in the process.

The response was disciplined:

- Built a counter-model showing the precise dollar impact of the revised terms ($1.6M shortfall to original LOI)

- Documented the specific value drivers being discounted

- Made clear the willingness to walk away—backed by documentation of alternative buyer interest

The buyer returned to the original terms within 72 hours.

Key Insight

The willingness to walk away is your strongest negotiating lever. But it only works if you've maintained alternatives and documented your value thesis. Emotional commitment without alternatives is how sellers leave money on the table.

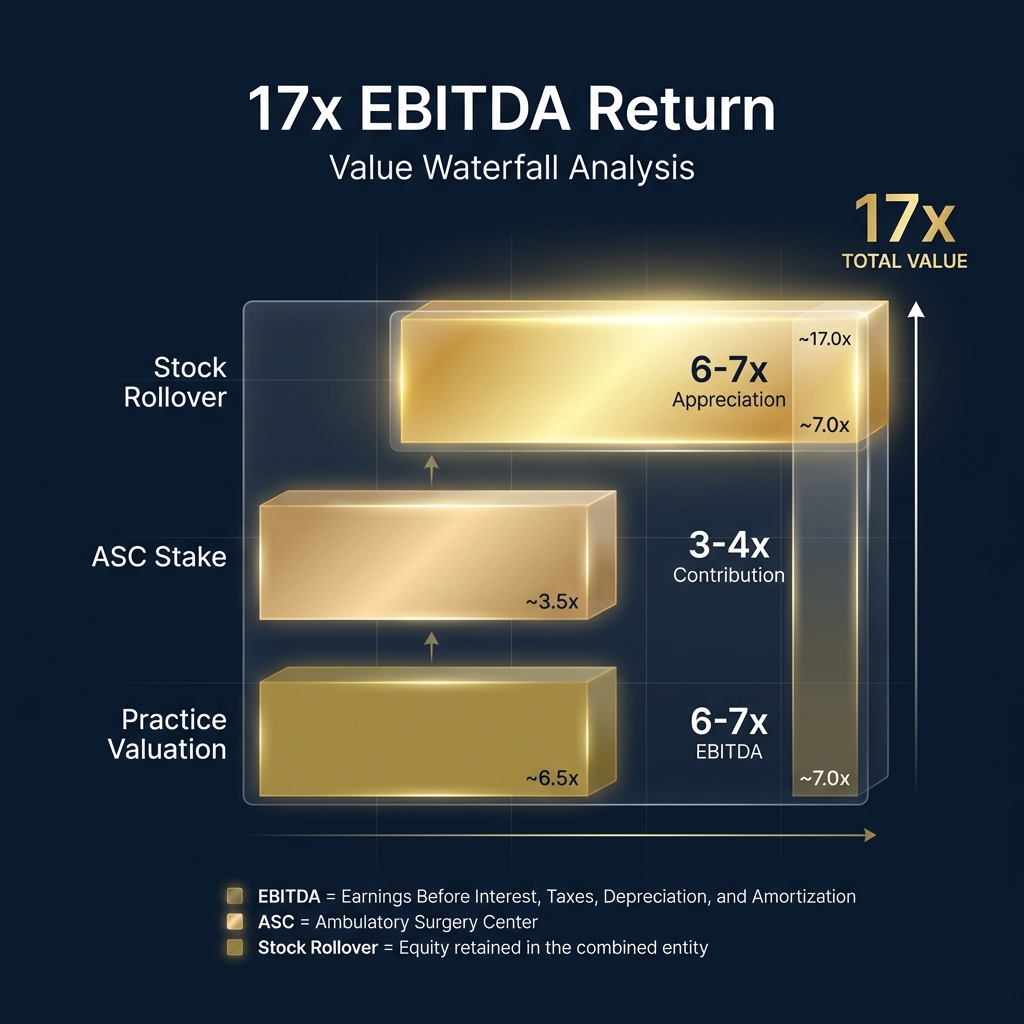

The 17x Formula

The effective 17x EBITDA return wasn't a single transaction—it was the combination of multiple value streams, structured to capture both immediate proceeds and long-term platform appreciation:

| Value Stream | Structure | Multiple Contribution |

|---|---|---|

| Practice Valuation | Cash at close + deferred payments | ~6-7x EBITDA |

| ASC Stake | Minority interest monetization | ~3-4x contribution |

| Stock Rollover | 80% reinvestment at platform exit | ~6-7x appreciation |

| Total Effective Return | Blended across all streams | ~17x EBITDA |

The mathematics of the rollover were critical. At 80% reinvestment with the platform's projected 10% CAGR over the employment period, the physician captured significant upside. At 50% reinvestment, the gap to original terms widened to $2.6M. The decision required confidence in the platform's execution—backed by documented growth trajectory and market analysis.

Deal Timeline

| Phase | Duration | Key Milestones |

|---|---|---|

| Initial Negotiation | 6 weeks | Counter-proposal at 15x on practice component; regulatory review of ASC structure |

| LOI Execution | 2 weeks | Term sheet signed; exclusivity granted |

| Due Diligence | 90 days | QofE engagement, chart audits, operational review, compliance verification |

| Retrade Defense | 1 week | Counter-model built; original terms restored |

| Definitive Documentation | 6 weeks | Purchase agreement, employment contracts, ancillary documents |

| Close | 1 week | Wire transfers; transition initiated |

Lessons for Practice Owners

- Unbundle your value. If you own ASC shares, have ancillary revenue streams, or have growth characteristics that fit a platform thesis—price each separately.

- Control the narrative with sell-side QofE. Letting the buyer run due diligence without independent validation invites price chips.

- Model the rollover carefully. Stock rollover is a bet on platform execution. Understand the math—both the upside and the risk of illiquidity.

- Be willing to walk. The strongest negotiating lever is a credible alternative. Maintain competitive tension throughout the process.

- Expect the retrade. It's not a matter of if, but when. Document your value thesis so you can respond with data, not emotion.

What's Your Practice Worth?

Start with a confidential valuation estimate. No obligation, no sales pitch—just the numbers.

Request Confidential ValuationExplore More

- Selling to Private Equity: How PE deals work and what to expect

- How Practice Valuation Works: Deep dive into EBITDA, multiples, and value drivers

- Apply for Advisory: See if your practice qualifies for institutional M&A support